🤓 Latest Submissions

Heatmapper

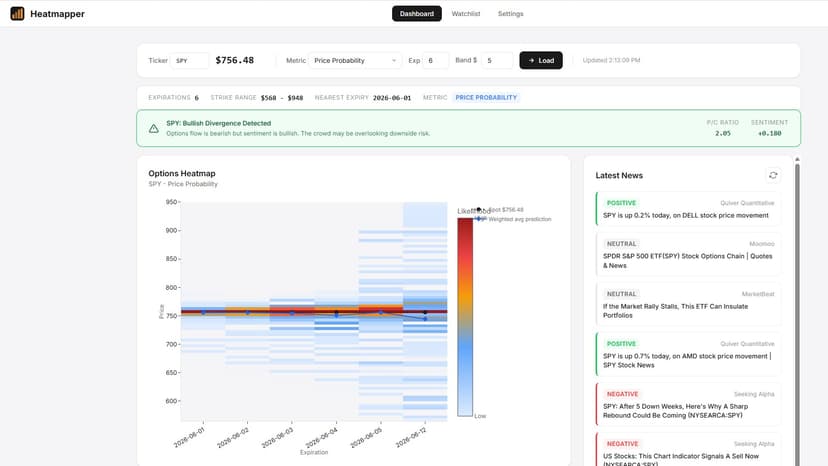

An options intelligence platform that ingests live option chains and inverts the market's pricing to surface what positioning actually implies for spot. Rather than assuming a symmetric lognormal from a single at-the-money volatility, it applies the Breeden–Litzenberger result — recovering the full risk-neutral density from the second derivative of call price with respect to strike — and prices each strike off its own point on the volatility smile, so the reconstructed distribution preserves the market's empirical skew and excess kurtosis (fat tails) instead of discarding them. On top of that, it analytically derives the higher-order Greeks (gamma, vanna) from Black–Scholes, since the vendor feed supplies implied vol and open interest but no sensitivities, and aggregates them across open interest under a dealer long-calls/short-puts convention to compute Gamma Exposure (GEX) and Vanna Exposure (VEX) — the dollar delta market-makers must re-hedge per 1% move in spot, and the analogous flow induced by shifts in implied volatility. The resulting heatmaps expose the gamma-flip level, call/put walls, and dealer hedging regime (volatility-suppressing vs. volatility-amplifying), letting a user read the mean-reversion vs. momentum structure of the tape and identify the strikes spot is likely to be pinned toward or repelled from — all overlaid with FinBERT-driven sentiment to flag positioning-vs-narrative divergences.

31 May 2026